- By Ankit Kumar

- Mon, 09 Sep 2024 08:22 PM (IST)

- Source:JND

The global economy today is marked by turbulence and uncertainty, drawing alarming comparisons to the late 1920s- a period that foreshadowed the Great Depression. With soaring stock markets, rising inequality and geopolitical tensions, economists and policymakers are increasingly concerned about the possibility of a severe economic downturn.

(Major elements of the world economy according to Gail Tverberg. These are human population, extracted resources including energy resources, and financial demand.)

Stock Market Surge: A Bubble Waiting To Burst?

The stock market’s meteoric rise over the past decade has been a hallmark of the current economic era. Fuelled by historically low interest rates, aggressive monetary policies and a flood of liquidity from central banks, stock indices have repeatedly hit record highs. This exuberance, however, bears an eerie resemblance to the speculative boom of the 1920s. During that time, easy access to credit and widespread speculation led to an inflated stock market bubble, which ultimately burst in 1929, triggering a cascade of economic failures.

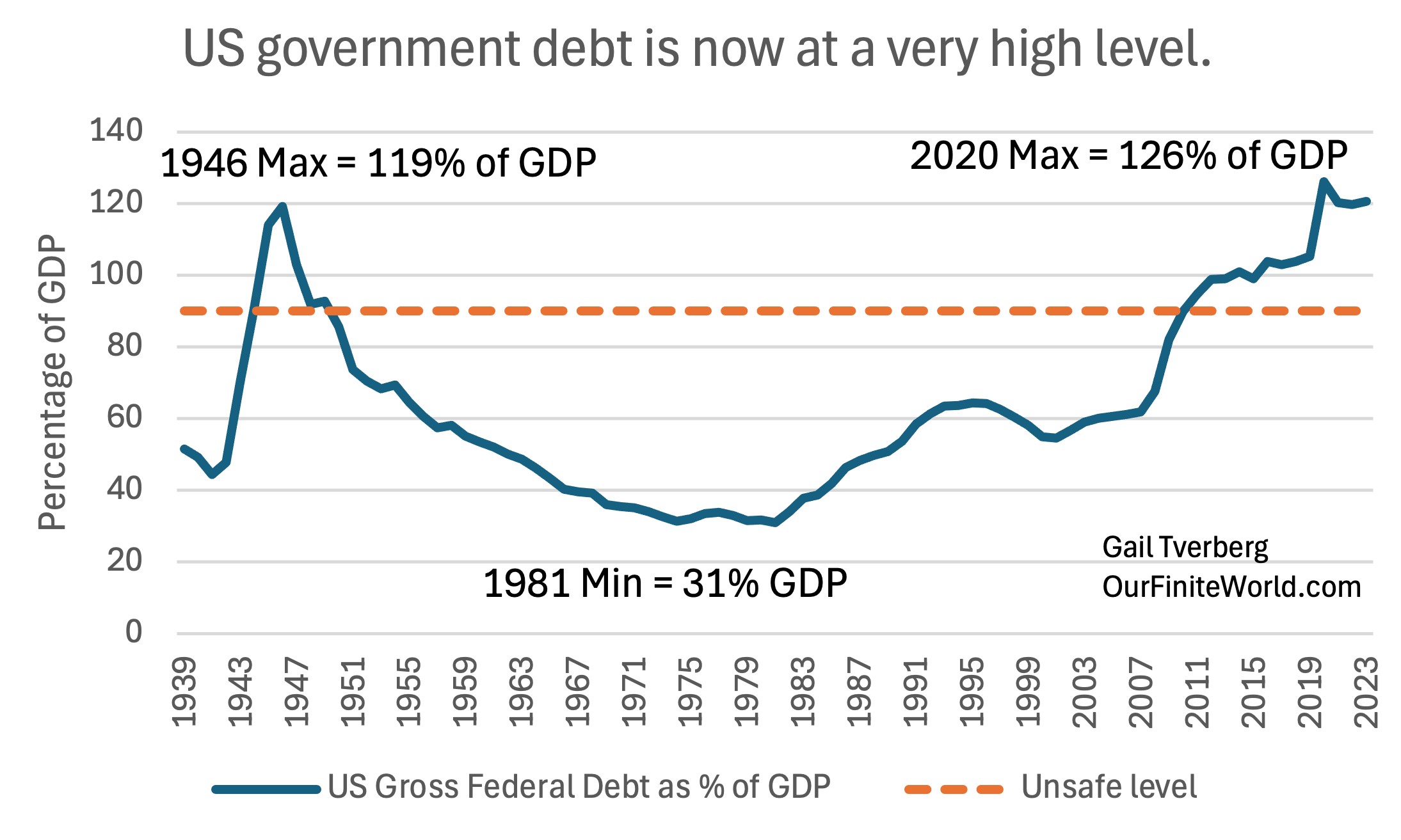

(US Gross Federal Debt as a percentage of GDP, based on data of the Federal Reserve of St. Louis. Unsafe level above 90% of GDP is based on an analysis by Reinhart and Rogoff.)

Today, there is growing concern that the stock market may be overvalued, with prices disconnected from underlying economic realities. Tech giants, in particular, have seen their valuations soar to unprecedented levels, driven by the digital economy’s dominance. However, the concentration of market power in a few large firms raises the spectre of a potential tech bubble. If these valuations prove unsustainable, a sudden market correction could have far-reaching consequences, potentially setting off a chain reaction similar to that of the late 1920s.

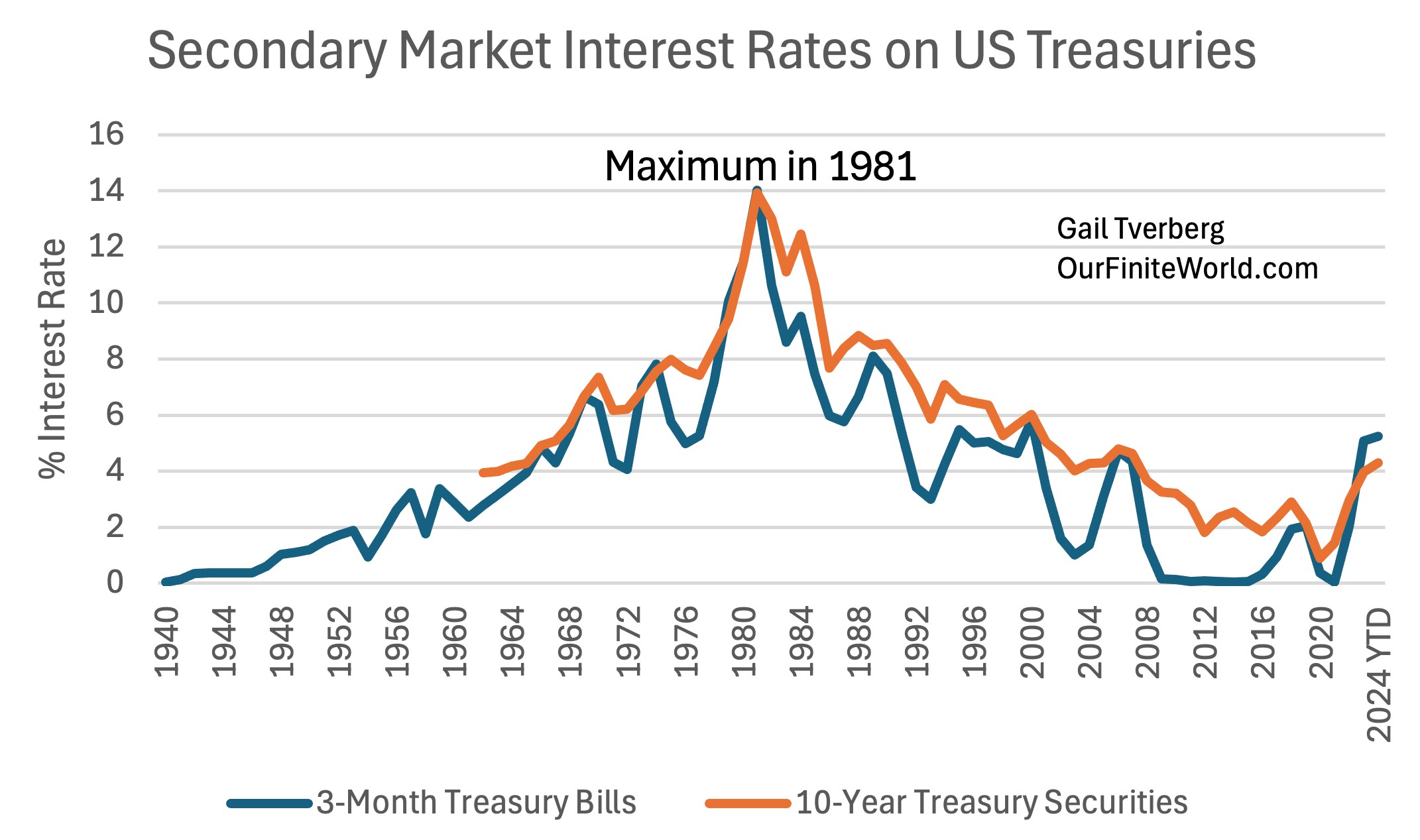

(Secondary market interest rates on 3-month US Treasury Bills and 10-year US Treasury Securities, based on data accessed through the Federal Reserve of St. Louis. Amounts for 1940 through 2023 are annual averages. Amount for 2024 YTD is average of January to July 2024 amounts.)

Rising Inequality: A Recurrent Theme

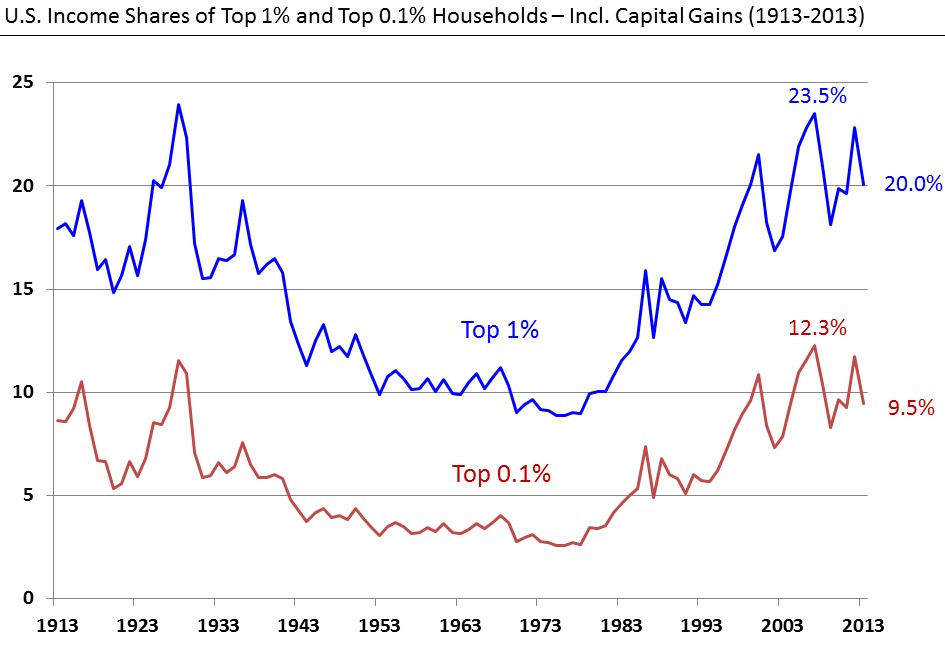

Economic inequality is another area where today’s economy mirrors the late 1920s. In the years leading up to the Great Depression, the gap between the wealthy and the working class widened significantly. The richest 1 per cent of Americans held a disproportionate share of the nation’s wealth, while the majority struggled with stagnant wages and declining living standards. This disparity contributed to the economic instability that followed the stock market crash, as consumer spending - a critical driver of economic growth - plummeted.

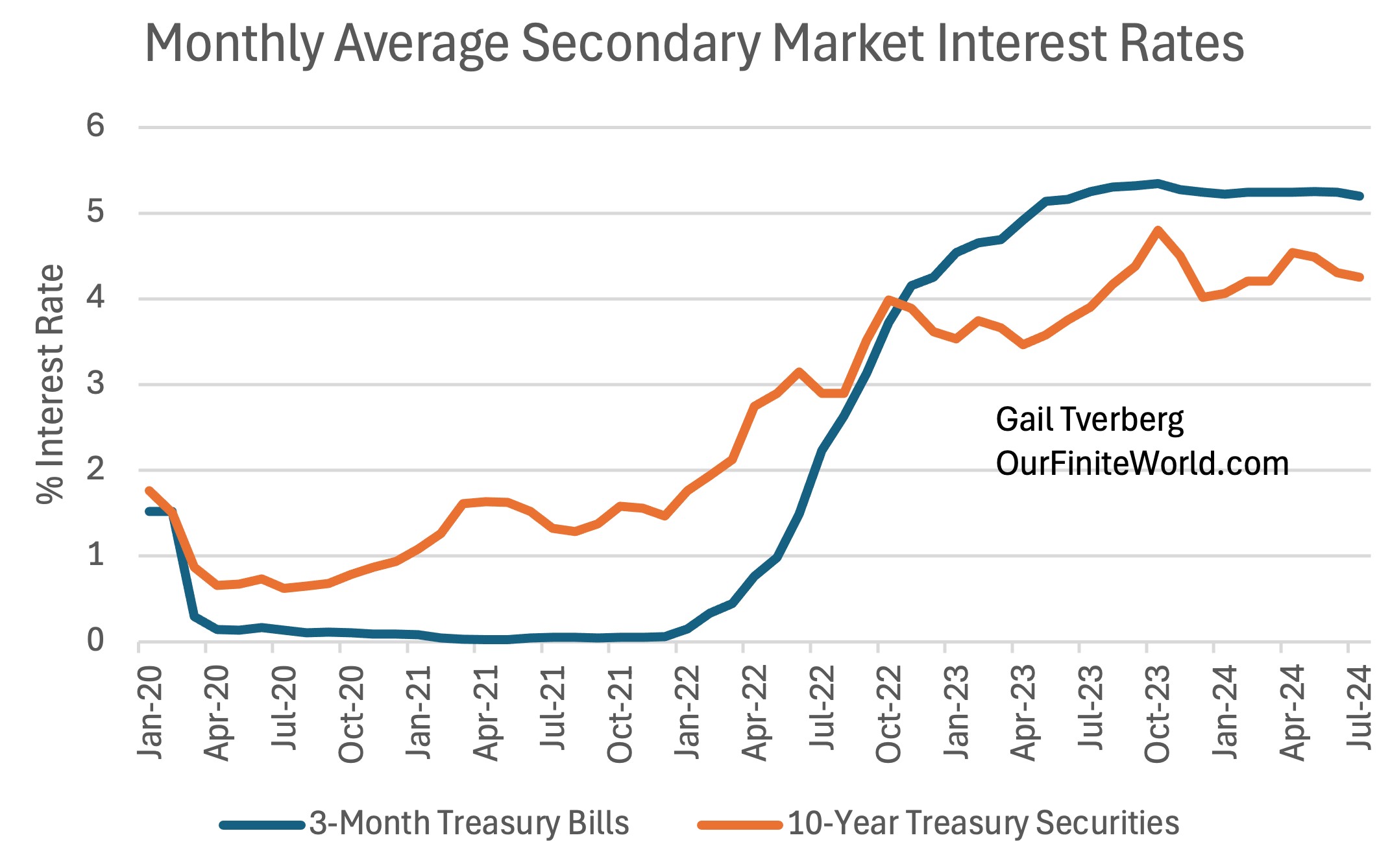

(Monthly average secondary market interest rates on 3-month US Treasury Bills and 10-year US Treasury Securities, based on data accessed through the Federal Reserve of St. Louis.)

In the 21st century, income and wealth inequality have once again reached alarming levels. According to recent studies, the top 1 per cent of the world’s population now controls nearly half of the global wealth. This concentration of wealth has been exacerbated by the Covid-19 pandemic, which disproportionately impacted low-income workers and small businesses. As the rich get richer, the middle and lower classes continue to struggle with rising costs of living, stagnant wages and limited access to opportunities for economic advancement.

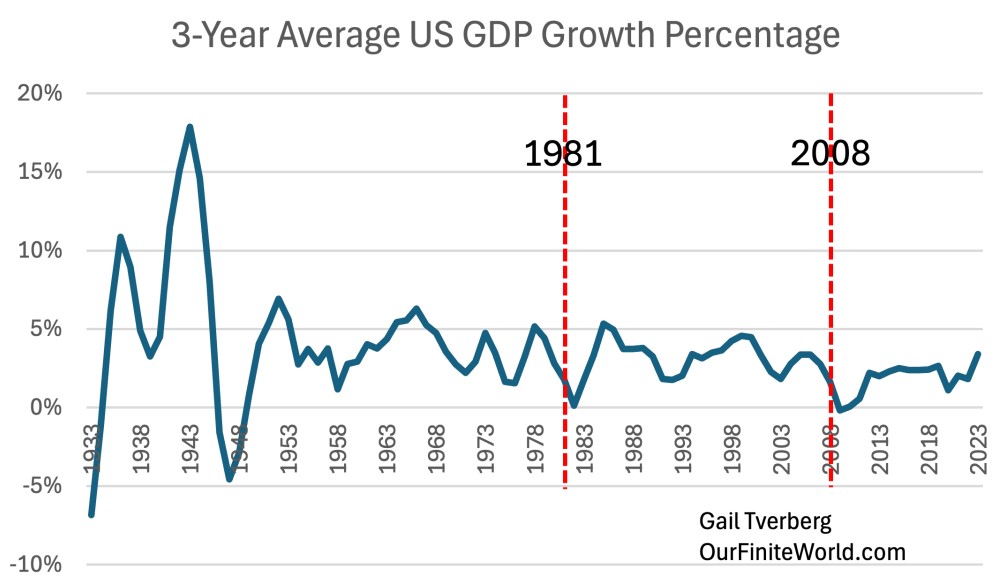

(Three-year average US inflation-adjusted GDP growth rates based on data of the US Bureau of Economic Analysis.)

Debt Overhang: A Ticking Time Bomb

High levels of debt are another striking similarity between the current economy and that of the late 1920s. In the run-up to the Great Depression, both consumers and businesses took on significant debt, driven by easy credit and the lure of quick profits in the stock market. When the market crashed, this debt became unmanageable, leading to widespread bankruptcies and a collapse in consumer spending.

Today, global debt levels have reached historic highs, surpassing USD 300 trillion in 2023. Governments, corporations and households alike have borrowed heavily to finance spending, investment and recovery efforts following the Covid-19 pandemic. While low interest rates have made this debt more affordable, there is a growing concern that rising interest rates - necessitated by efforts to combat inflation - could make this debt burden unsustainable. A wave of defaults, particularly in emerging markets and heavily indebted sectors, could trigger a financial crisis that reverberates across the global economy.

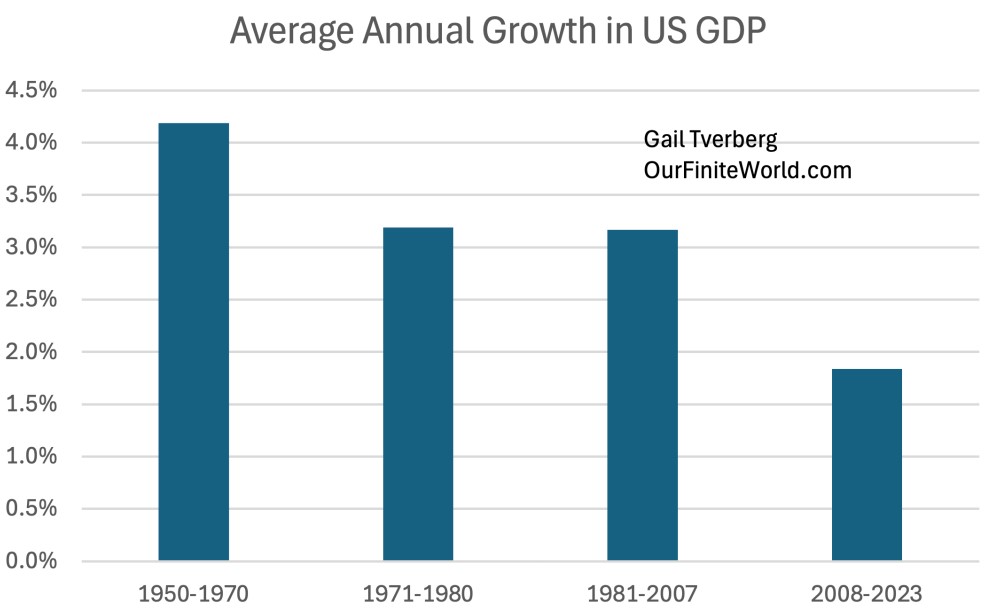

(Average annual US GDP growth rates based on data of the US Bureau of Economic Activity.)

Role Of Technology

One of the most significant differences between today’s economy and that of the 1920s is the role of technology. The digital revolution has transformed the global economy, creating new industries, jobs and opportunities for innovation. Companies like Amazon, Google and Apple have not only become economic powerhouses but have also reshaped how businesses operate and consumers engage with the market.

However, this technological dominance also presents risks. The rapid pace of technological change has disrupted traditional industries, leading to job losses and economic dislocation in sectors such as manufacturing and retail. Moreover, the concentration of economic power in a few tech giants raises concerns about market distortions and the potential for a tech bubble. If these companies were to experience a sudden decline in value, the impact could be felt across the global economy, potentially triggering a broader economic downturn.

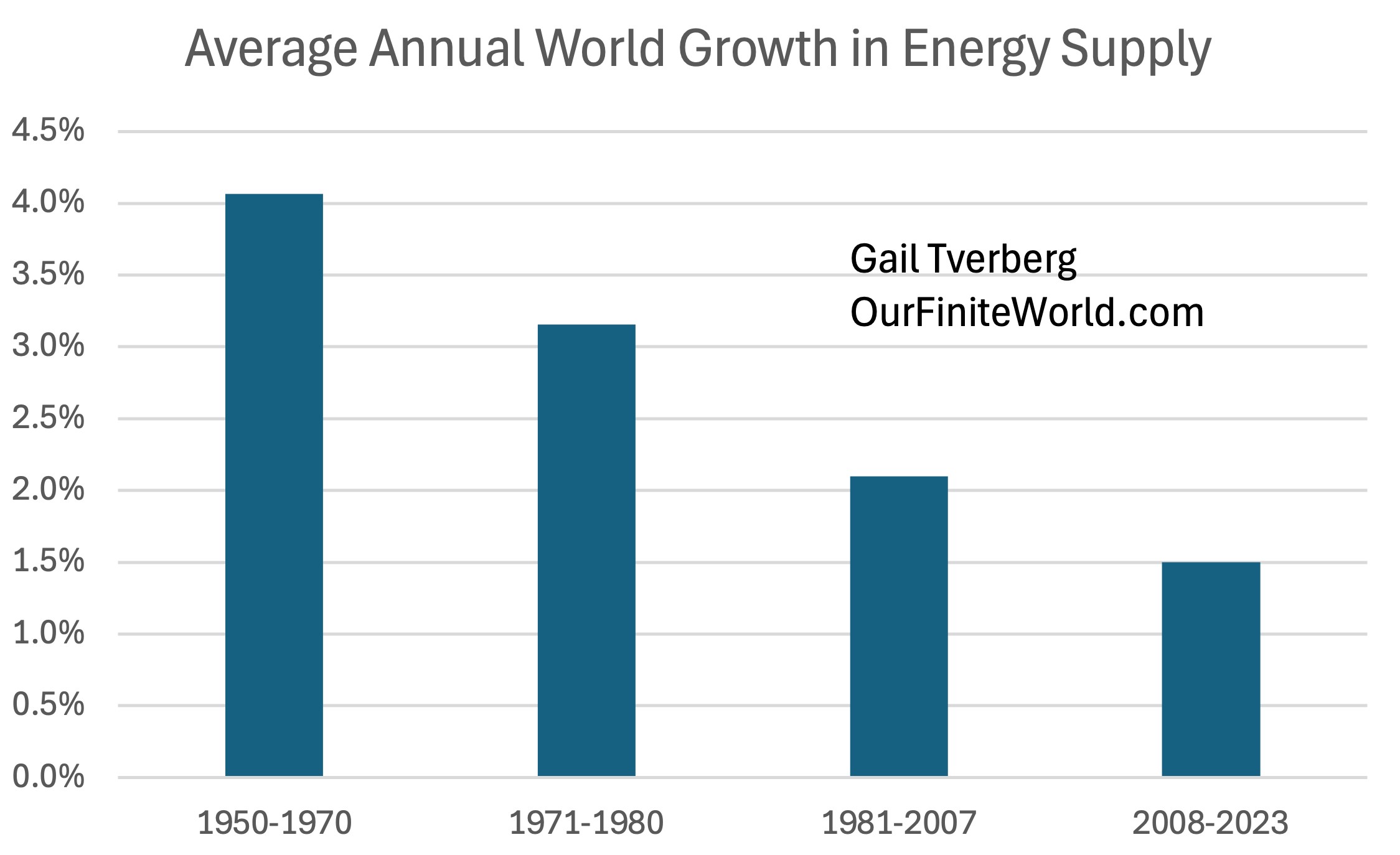

(Annual rate of increase in energy consumption growth for the earliest grouping is based on data provided by Vaclav Smil in the Appendix to Energy Transitions. Average rates of increase for later periods are calculated from data of the 2024 Statistical Review of World Energy, by the Energy Institute.)

Geopolitical Tensions

Geopolitical risks have always played a significant role in shaping economic outcomes and today is no different. In the late 1920s, rising nationalism and protectionism contributed to the economic collapse that followed the stock market crash. Tariffs, trade barriers and a lack of international cooperation exacerbated the economic downturn, leading to a prolonged period of global stagnation.

In the current era, geopolitical tensions are once again on the rise. The ongoing trade war between the United States and China, coupled with tensions in the South China Sea, has raised the spectre of a global trade disruption. The conflict in Ukraine and the broader struggle between NATO and Russia have further destabilised global markets, leading to volatility in energy prices and uncertainty in supply chains. These geopolitical risks could act as a catalyst for economic instability, particularly if they lead to a breakdown in international trade or a significant disruption in global supply chains.

(U. S. Income Shares of Top 1% and Top 0.1%, Wikipedia exhibit by Piketty and Saez.)

Inflation And Interest Rates

Inflation has emerged as one of the most pressing economic challenges of our time. Unlike the deflationary pressures of the 1920s, today’s economy is grappling with rising prices, driven by supply chain disruptions, increased demand and the lingering effects of the COVID-19 pandemic. Central banks around the world, including the Federal Reserve and the European Central Bank, have begun to raise interest rates in an effort to curb inflation.

However, there is a delicate balance to be struck. Raising interest rates too quickly could stifle economic growth and lead to a sharp correction in asset prices, similar to the events of 1929. On the other hand, failing to control inflation could erode purchasing power, reduce consumer confidence and trigger a prolonged economic downturn. The challenge for policymakers is to navigate this tightrope carefully, ensuring that inflation is kept in check without derailing the economic recovery.

(Representation of an economy that is growing up until not long after 2020, and shrinking thereafter, by Gail Tverberg.)

Energy Crisis

Energy markets are another area of concern that could potentially trigger a global recession. The ongoing conflict in Ukraine has led to significant disruptions in energy supplies, particularly in Europe, which is heavily reliant on Russian oil and gas. Sanctions and counter-sanctions have led to skyrocketing energy prices, contributing to inflation and increasing the cost of living for consumers around the world.

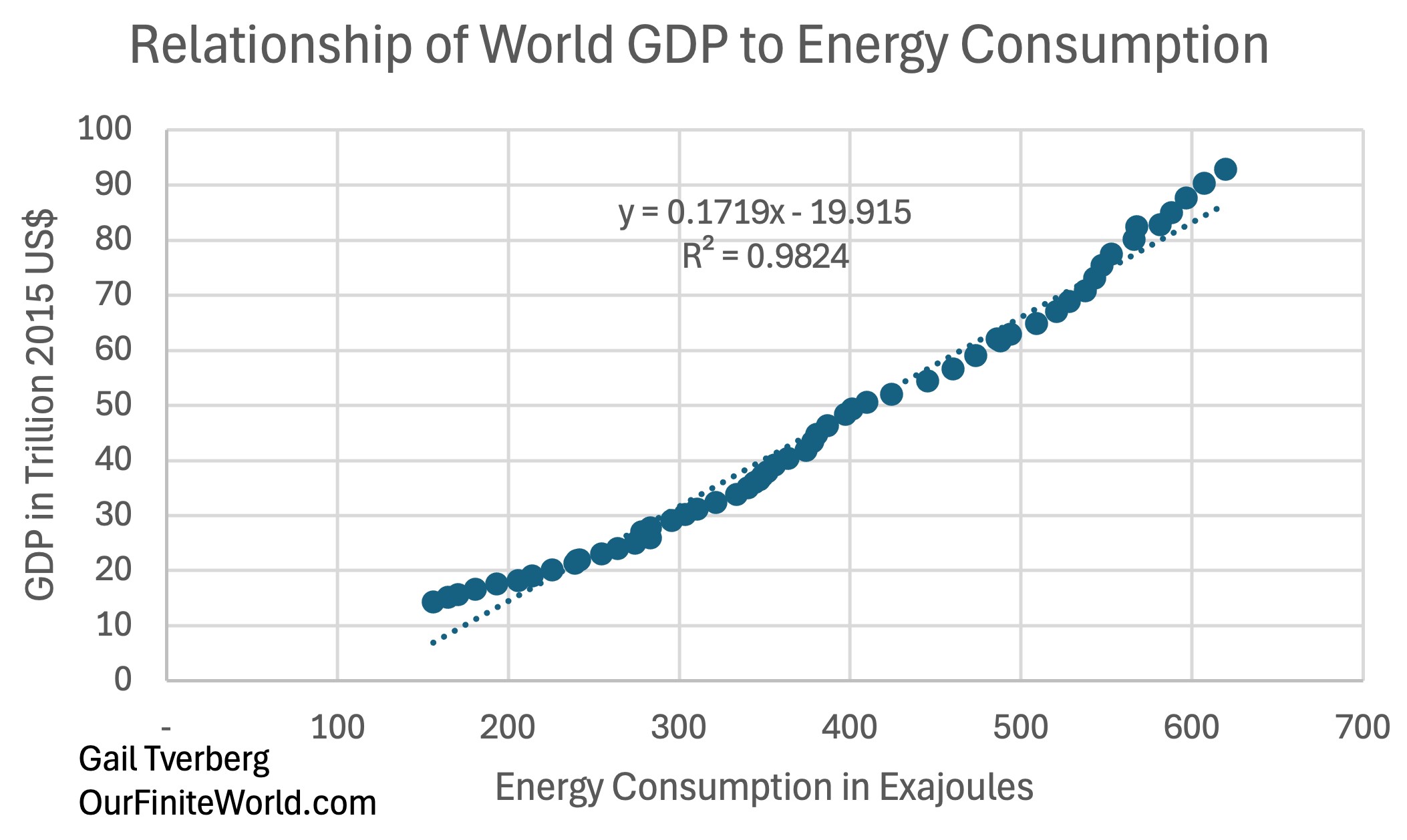

(Relationship between inflation-adjusted world GDP based on data of the World Bank and energy consumption based on data of the 2024 Statistical Review of World Energy, published by the Energy Institute.)

Moreover, the transition to renewable energy, while essential for combating climate change, presents its own set of challenges. The shift away from fossil fuels requires significant investment in infrastructure, technology and innovation. If not managed carefully, this transition could lead to energy shortages, increased costs and further economic instability, particularly in regions heavily dependent on fossil fuels.

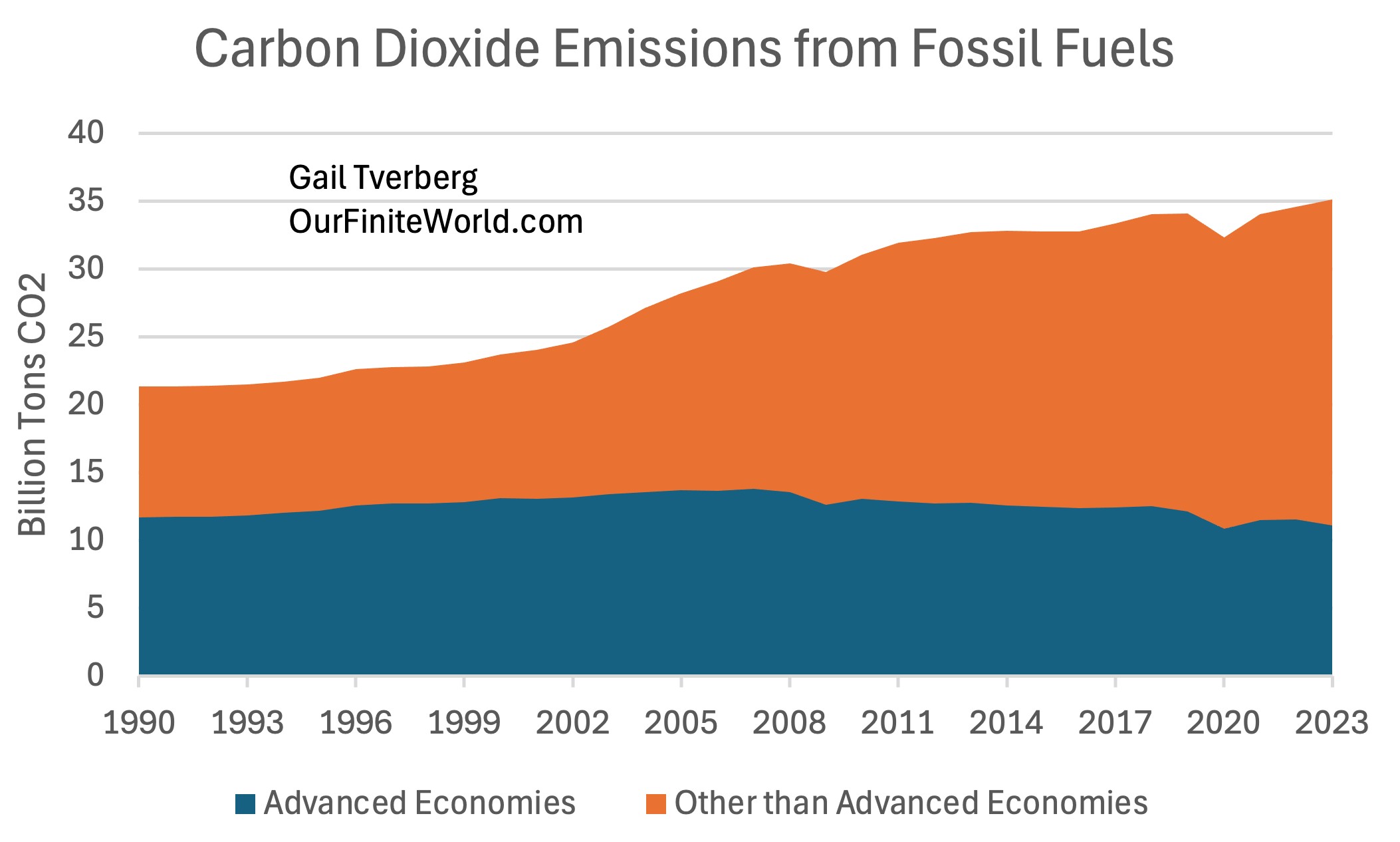

(Carbon dioxide emissions for Advanced Economies (members of the Organization for Economic Co-Operation and Development) versus all others, based on data of the 2024 Statistical Review of World Energy published by the Energy Institute.)

Where Is The Global Economy Headed?

Given the multitude of challenges facing the global economy, predicting the future is fraught with uncertainty. Several scenarios could unfold in the coming years, each with its own set of implications for the global economy.

1. Soft Landing: In a best-case scenario, the global economy could achieve a soft landing, with inflation gradually easing, supply chains stabilising and economic growth rebounding. This would require careful management of monetary policies, continued fiscal support and effective international cooperation to address global challenges such as climate change, energy security and geopolitical risks.

2. Severe Recession: A more pessimistic scenario could involve a sharp economic downturn, triggered by a sudden financial shock, a collapse in asset prices, or a major geopolitical crisis. In this scenario, the global economy could slide into a severe recession, potentially leading to a prolonged period of economic stagnation akin to the Great Depression.

3. Stagflation: A third possibility is that the global economy could enter a period of stagflation, characterised by stagnant economic growth, high unemployment and persistent inflation. This scenario would present significant challenges for policymakers, as traditional tools for managing inflation and stimulating growth may prove ineffective.